In 2017, the corrupt president of South Korea, Park Geun-hye, was lawfully removed by a national uprising of orderly, peaceful protesters. Ordinary housewives, business people and manual laborers gathered in public squares across the nation, held candlelight vigils and cleaned up their litter when they were done. In 1998, when South Korea suffered a liquidity crisis and had to depend on the IMF’s typically harsh rescue measures, ordinary citizens donated 227 tons of gold to the government in order to pay off national debts and restore national honor. In 2020, the eruption of COVID19 threatened to cripple the economy but ordinary people quickly and effectively adopted social distancing and tracing programs that have, without any official lockdowns, held the Korean infection rate to about 1/300th of the infection rate in lockdown-riddled places like England and California. This is the sort of voting population that Renaissance and classical thinkers like Edward Gibbon, Cicero, Niccolo Machiavelli and Dante Alighieri would consider “worthy of freedom” in the Greco-Roman, citizen-of-the-Republic sense of the word.

It’s less certain we can say the same things about many Western countries. As is becoming something of a theme post-2020, elites and bureaucrats seem to be outperforming elected officials, citizens’ groups and regular voters. We’ve already discussed the generally laudable ways business elites and unelected bureaucrats handled COVID and the Floyd Protests compared to the questionable actions undertaken by activists, protesters, elected officials, union members and, in short, anyone connected to the little guy.

If you don’t want to go back and read that article, the short version is this: giant corporations and unelected officials brought us vaccines in record time, stopped what appear to have been several coup attempts, fought effectively against attempts to politicize the justice system, kept the hospital system afloat even while it was being massively overloaded and supported freedoms to assemble and freedom to speak even as protesters tried to murder them.

On the other hand, citizens’ groups performed really poorly. Police unions blocked badly needed reform. Racial justice protesters demanded unrealistic and harmful measures like “defund” and drove their point home by crushing policemen under SUVs and lighting practically every major US city on fire. Freedom protesters spread COVID in the name of liberty and ordinary citizens attacked citizens who were trying to contain the outbreak. Elected officials attempted coups, cracked down on the press and burned forests. Conspiracy theorists did their best to overwhelm hospitals and the elderly and sick were told to embrace a more Darwinian outlook. I don’t know what Gibbon, Cicero, Machiavelli and Alighieri would say about many of these Western citizens, but I doubt “worthy of freedom” would be high on the list.

I mention this because the little guy can be noble, but he sure as hell isn’t automatically noble. Rights and lawfulness can flow from the bottom up, but likewise, they can flow from the top down. Insanity and self-destruction are possible in the elites, but they are certainly not confined to the high and mighty.

The world of economics has recently manifested this little guy, big guy dynamic in the ongoing “elite” preference for fiat currency and the little guy’s grassroots gold and bitcoin movements. As such, it’s perhaps wise to see if the economic little guys in this controversy are more aligned with Korean candlelight protesters or Texas anti-vaxxers.

(Thanks to M. Talmage Moorehead for inspiring this article.)

Explanation of the gold standard’s problems

When discussing the virtues of a gold standard, advocates almost always mention a variation on the theme of “realness.” The idea that gold is real because it’s metal/shiny/rare/good-at-conducting-electricity/whatever and that all modern currencies are not real because they are made of paper is, on many levels, mistaken. On a very basic level, neither a piece of paper nor a chunk of metal can be classed as anything other than tangible. If we move onto electronic representations of money, our gold bug is still missing the most fundamental aspect of capitalism – things have value because we say they have value. Gold is no more “naturally valuable” than any other thing. A dollar is no less “naturally valuable” than anything else with a limited supply and market demand. This argument about realness has no merit and, rather than the “real capitalist” vibe gold advocates are normally shooting for, betrays a misunderstanding of how valuation works.

There is also the notion of collateral. The idea here being that precious metal-backed currencies are like the collateral we put up when we get a mortgage. The first and most obvious point to make is difference between bank-to-customer transactions and the issuance of paper currency. Banks demand security for loans because you are expected to pay back the loan (plus interest), and in the eventuality that you cannot, it will instead relieve you of your collateral. A government issues currency partially to pay for things but mostly to facilitate trade. This isn’t quite apples and hand grenades, but it is apples and apple-scented hand grenades.

The valid point gold-bugs and anti-fiat currency types make is that, absent “collateral,” governments can print money willy-nilly and create massive inflation spikes. This is a possibility, and some poorly run dictatorships, cough – Mugabe’s Zimbabwe – cough, have indeed abused their fiat currencies in exactly the way economic populists types predict. However, in democracies and especially in democracies with responsible voting populations, the predicted inflation spikes are very rare, and in fact much less common than spikes caused by precious metal backed currencies.

At this point we need to discuss the “intrinsic value” of fixed currencies and why they, in practice, provide almost none of the stability they supposedly exist for. A given amount of currency represents the value of a specific amount of productivity at a specific moment in time according to market forces. For legal tender, its guarantee comes in the fact that it will be accepted by the government for payment of taxes, the purchasing of government debt, the fact that a debtor must legally accept it as payment of debt. All of this generates genuine market value – indeed imbues the currency (gold coins or paper bills or sea shells) with powers far beyond carrying gold dust around in your pocket. In other words, while it is true that fiat currencies only have value because we say so, the basic structure of supply and demand makes that true of practically everything.

We can see the evidence for this by observing how, during the heights of the 2008 recession, the demand for US government bonds increased rapidly. Market forces dictate the value of a gold or silver bar sitting in a vault as much as they do a dollar note: they have no intrinsic value beyond that. You cannot use a silver certificate or a buck note made of cloth to dig a well, or harvest corn, or scan things through a till, or play sports or decide matters of law. They are not being used to do anything, they are simply a limited resource being used to represent a certain amount of productivity at a specific moment in time. The legal part of legal tender is where currency gains its market value, not the backing (if any). Indeed, it is difficult to imagine a bigger economic calamity than the holders of a backed currency suddenly exchanging their currency for that backing. The few times backed currency holders did exchange their currency for the backing in large amounts, enormous economic depressions followed.

The amount of productivity a given unit of currency represents will fluctuate for reasons beyond mere changes in productivity however. When a currency is pegged to a precious metal then the discovery of more of the precious metal will cause global inflation, and when a ship laden with gold sinks to the seabed, then the opposite occurs, as examples. When Spain became flush with gold and silver from its conquest of the new world, it caused such intensive inflation that the peso became worthless with ludicrous rapidity, and Spain became a poor country within the last few decades of the 16th century because of – rather than in spite of – having amassed prodigious amounts of precious metals – around 1.5 trillion dollars worth in modern currency – in a very short space of time. In fact, this influx of currency backing gold, and the massive trade imbalances that went along with it, spread like a contagion across much of western Europe, leaving huge inflationary spikes behind in its wake. The “stability” of “real” gold, in Spain and Europe, vanished as soon as the supply of gold expanded, leading to hyper-inflationary spikes of the sort to make Mugabe blush.

The western United States underwent the same problems during the gold rush; if there are more gold coins about, but there is no increase in productivity, then the value of the gold simply diminishes – inflation. Similarly inflation will fluctuate dramatically through simple and basic trade imbalances: gold will flow out of a nation as a country exports more, and will flow into the system when it exports less. Because the value of the currency and the value of the precious metal are not naturally correlated, the government must artificially assign a value for the backed currency and then hope it guessed right. Thus, rather than freeing the currency from vile government interference, the gold backing forces some central body to assign a value to the currency it would not under a fiat system. Sometimes, such as with the UK in the inter-war years, the government sets the value of its gold standard comically, terribly wrong, and strangles trade.

Precious-metal backed currencies are also really, really vulnerable to runs and panics. During an economic crisis, people tend to hoard gold, silver and the like. With a fiat currency, this isn’t a particular problem since it is merely a single (not very important) commodity, not the means of exchange, that’s being pulled out of the economy and stuffed under the mattress. However, with a gold-backed currency the problem is profound. The removal of gold by spooked consumers in a backed currency system doesn’t just create a price spike in a single, not very important commodity, but directly affects the transactions of everyone using the currency. The means of exchange dries up in these situations, seriously undermining the average consumer’s ability to sell labor and buy bread, sell corn and buy gasoline, sell insurance and buy furniture.

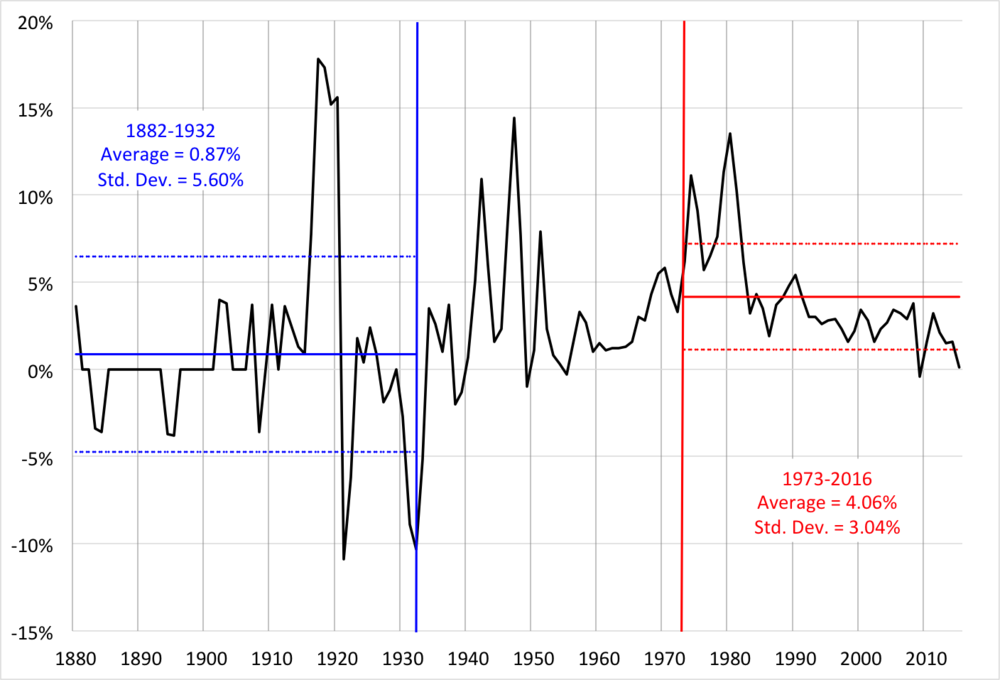

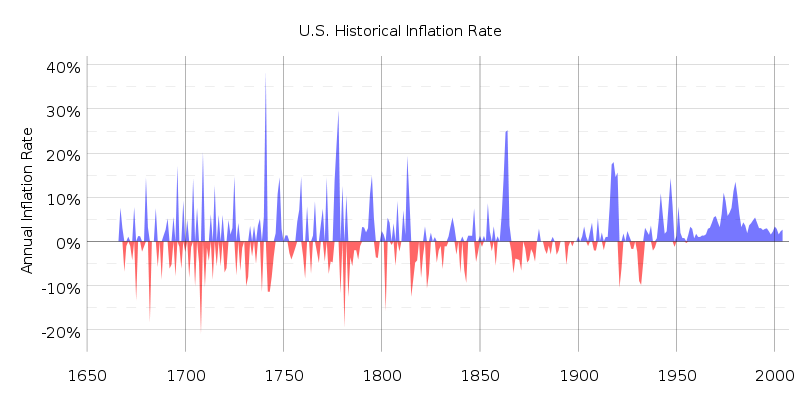

It is important, at this juncture, to remember all those passionately expressed and comically wrong predictions of inflation floating around in 2008-2009. The failure of Peter Schiff‘s and Ron Paul’s predictions provide an excellent means for rejecting their gold bug arguments into the future. Further, an examination of history shows that the gold standard era had, contrary to the tranquility predicted by Schiff, Paul and others, massive swings in inflation/deflation rates.

When an economy is overheating and vulnerable to both bubbles and inflation, gold-backed currency tends to flow in that direction. Because a bubbling economy demands more of everything, gold and currency MUST move towards these economies. Because the gold is also the currency we must, as the Spanish discovered, see an increased inflation rate as well. This has the effect of making almost any growth period a corresponding period of inflation. See the 40% inflation rate spikes in both the US and UK historical charts while under the supposedly “secure” gold standard.

Worse, the gold standard locks in the opposite effect in contracting economies. When a nation experiences a slowdown, its demand for both gold and currency falls and they experience a net outflow of money. This causes an increase in the value of currency and a decrease in the average price of goods. This is exactly the opposite of responsible, counter-cyclical monetary policy. It is gasoline on the inflation fire during overheating periods and liquid nitrogen on the already hypothermic conditions of a depression. This means deflation. Deflation is, correspondingly, a difficult to cure death spiral of contracting demand and shrinking output the type of which caused the worst sufferings in both the Great Depression and Great Recession. In other words, a thing we should do almost anything to avoid.

The Gold Standard and Crypto Currencies

Crypto currencies are in many, but not all, ways similar to the gold standard. Let’s start with the similarities:

- It is, like gold, theoretically free from central banks. This gives many people wholesome “freedom” feelings, though I question the logic. More practically speaking, this partial independence from central banks means that there is also a partial independence from future Mugabes. That said, this independence is only partial because, just like the gold standard problems mentioned above, a cryptocurrency will need to be assigned a value by a central authority the instant you try to use it to pay taxes or exchange it for Japanese yen.

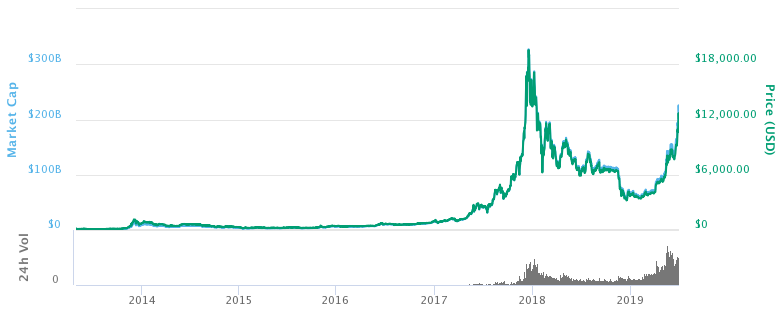

- It is, like the gold standard, very unstable. Bitcoin has seen inflation and deflation in the thousands of percent ranges. This makes it a potentially useful as an investment in the “bigger fool” sense of investment. However, it also makes cryptocurrencies dubious for many types of exchange since most vendors (including the author of a brand new novel “Joshua and the Chosen People”) would be very reluctant to accept payment in a currency with inflation and deflation charts that need to be measured on the logarithmic scale.

- It is, like the gold standard, “mined.” This is the basis of cryptocurrency’s relative independence but, like the Spanish in the late 16th century, the vagaries of mining make it unpredictable and vulnerable to runs, crashes (literal or metaphorical) and panics.

There are, however, a couple of differences between cryptocurrency and precious metal backed currency that bear mentioning:

- It is in some ways more secure. Blockchain technology, which I’m not qualified to explain in any detail, is claimed by many serious and intelligent people to be very secure in ways fiat currencies are not, particularly when you transfer it across national boarders. The “mining” of cryptocurrency is also, theoretically, more resistant to supply shocks than gold. That is, it’s harder so far to hit a mother-load and flood the market with cryptocurrency than it is to do so with a gold rush or imperial adventure in South America.

- It is in some ways less secure. While there is nothing to stop us deciding we no longer care about gold, or that we care about it less, it is difficult to imagine North Korean hackers deleting the world’s supply of precious metals.

Overall, however, the cryptocurrency movement seems to have a great deal of similarity with the old gold standard. This means we probably shouldn’t depend too much on cryptocurrencies for our means of exchange, though as a sideshow or speculative market there’s really not problem. Likewise, cryptocurrencies are becoming more and more responsible – many now peg themselves to fiat currencies – and the potentially better security might allow for larger-scale adoption in the future.

That said, I fear a large part of the appeal is a vague, freeberation, stick it to the man sort of feeling. In this sense, the man really hasn’t done anything to deserve the stick.

{kind=link}

{kind=link}