Explanation of the gold standard’s problems.

When discussing the virtues of a gold standard, advocates almost always lead with a variation on this question. Why don’t governments operate with collateral – ie a gold or silver backing – in their money printing operations like citizens do when getting a loan? If by some chance, the advocate does not use this argument, he or she will assuredly move onto the transparently foolish notion of “realness.”

The idea that gold is real because it’s metal/shiny/rare/good-at-conducting-electricity/whatever and that all modern currencies are not real because they are made of paper is, on many levels, ridiculous. On a very basic level, neither a piece of paper nor a chunk of metal can be classed as anything other than tangible. If we move onto electronic representations of money, our gold bug is still missing the most fundamental aspect of capitalism – things have value because we say they have value. Gold is no more “naturally valuable” than any other thing. A dollar is no less “naturally valuable” than anything else with a limited supply and market demand. This argument about realness has no merit and, rather than the “real capitalist” vibe gold advocates are normally shooting for, betrays a profound ignorance of how valuation works.

As for the notion of collateral, the first and most obvious point to make is the lack of allegory between bank-to-customer transactions and the issuance of paper currency. Banks demand security for loans because you are expected to pay back the loan (plus interest), and in the eventuality that you cannot, it will instead relieve you of your collateral. A government issues currency as legal tender to facilitate trade. Apples =/= hand grenades.

The second obvious point is the obsession with intrinsic value and misunderstanding of inflation. I will unpack all of this because I think the development of economies from pegged exchange rates was both fascinating and necessary.

A given amount of currency represents the value of a specific amount of productivity at a specific moment in time according to market forces. For legal tender, its guarantee comes in the fact that it will be accepted by the government for payment of taxes, the purchasing of government debt, the fact that a debtor must legally accept it as payment of debt. All of this generates genuine market value – indeed imbues the currency (gold coins or paper bills or sea shells) with powers far beyond carrying gold dust around in your pocket. We can see the evidence for this by observing how, during the heights of the recession, the demand for US government bonds increased rapidly. Market forces dictate the value of a gold or silver bar sitting in a vault as much as they do a dollar note: they have no intrinsic value beyond that. You cannot use a silver certificate or a buck note made of cloth to dig a well, or harvest corn, or scan things through a till, or play sports or decide matters of law. They are not being used to do anything, they are simply a limited resource being used to represent a certain amount of productivity at a specific moment in time. The legal part of legal tender is where currency gains its market value, not the backing (if any). Indeed, it is difficult to imagine a bigger economic calamity than the holders of a backed currency suddenly exchanging their currency for that backing.

The amount of productivity a given unit of currency represents will fluctuate for reasons beyond mere changes in productivity however. When a currency is pegged to a precious metal then the discovery of more of the precious metal will cause global inflation, and when a ship laden with gold sinks to the seabed, then the opposite occurs, as examples. When Spain became flush with gold and silver from its rape of the new world, it caused such intensive inflation that the peso became worthless with ludicrous rapidity, and Spain became a poor country within the last few decades of the 16th century because of – rather than in spite of – having amassed prodigious amounts of precious metals (perhaps more than 1.5 trillion dollars worth in modern currency) in a very short space of time. In fact, this influx of currency backing gold, and the massive trade imbalances that went along with it, spread like a contagion across much of western Europe, leaving huge inflationary spikes behind in its wake. The western United States underwent the same problems during the gold rush; if there are more gold coins about, but there is no increase in productivity, then the value of the gold simply diminishes – inflation. Similarly inflation will fluctuate dramatically through simple and basic trade imbalances: gold will flow out of a nation as a country exports more, and will flow into the system when it exports less. Because the value of the currency and the value of the precious metal are not naturally corellated, the government must artificially assign a value for the backed currency and then hope it guessed right. This (in combination with some other things, such as an especial vulnerability to speculation and runs) intrinsically results in wildly fluctuating prices, and sometimes, such as with the UK in the inter-war years, the government sets the value of its gold standard comically, terribly wrong, and strangles trade.

A government is considerably more flexible in being able to print or save fiat currency (this is most commonly done through the sale and purchase of assets through a central bank) than in getting its hands on gold when it needs it. The major break on a government just printing loads of money to pay off its debts is that it scares away investors, drives up interest rates and has other effects that make it generally harder to borrow into the long term (because the value of productivity it represents decreases and businesses are not quite thick enough to keep falling for it). Hence why the fed has continued to pursue a policy of extremely low inflation, even dipping into deflation, completely contrary to the beliefs of internet libertarians and professional idiot Ron Paul.

It is important, at this juncture, to remember all those passionately made and comically wrong predictions of inflation floating around in 2008-2009. The failure of people like Peter Schiff and Ron Paul’s predictions have, predictably, not slowed them down at all nor have these failed predictions caused a wave of self-reflection in their followers. It therefor falls to us to ignore these people the next time the news media decides to take them seriously.

There are more problems with fixed exchange rates which make the idea that they are supported by ‘hard assets’ false, but I think, at this point, I need only point to the most salient. The one supposed benefit of a fixed exchange rate compared to a fiat currency – the belief that they are secure because they are supported on a 1:1 basis by their reserves – is also the belief that a government will stick to the standard. As everyone on this planet knows, no sane government, and no sane public, would want to hold onto it during a financial crisis, and they will come off it. Thus the prestige and security of a fixed standard is untrue and meaningless. We have profited from abandoning the silly premise.

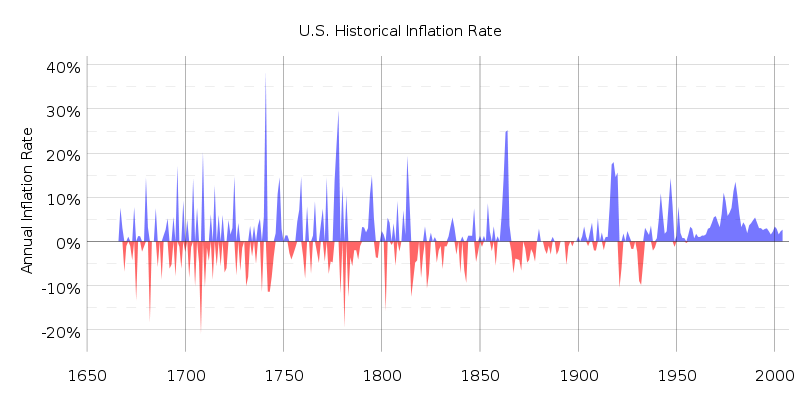

Further, an examination of history shows that the gold standard era had, contrary to the tranquility predicted by Schiff, Paul and others, massive swings in inflation/deflation rates. This has a great deal to do with the way money flows when the entire world has asset-pegged currencies.

When an economy is overheating and vulnerable to both bubbles and inflation, gold-backed currency tends to flow in that direction. Because a bubbling economy demands more of everything, gold and currency MUST move towards these economies. Because the gold is also the currency we must, as the Spanish discovered, see an increased inflation rate as well. This has the effect of making almost any growth period a corresponding period of inflation. See the 40% inflation rate spikes in both the US and UK historical charts while under the supposedly “secure” gold standard.

Worse, the gold standard locks in the opposite effect in contracting economies. When a nation experiences a slowdown, its demand for both gold and currency falls and they experience a net outflow of money. This causes an increase in the value of currency and a decrease in the average price of goods. Ideally, the bubbling country is supposed to inflate its currency so that the amount of gold and the amount of currency match. This isn’t so hard. However, a country in recession is supposed to worsen its unemployment and GDP by cutting the currency supply. This means deflation. Deflation is, correspondingly, a difficult to cure death spiral of contracting demand and shrinking output the type of which caused the worst sufferings in both the Great Depression and Great Recession. In other words, a thing we should do almost anything to avoid.

The whole effect with a globally pegged currency, then, is to make the bubbles bubblier and the recessions into depressions. Internet libertarians have a hard time with this because their desired conclusion “government is always bad” matters more than any theoretical framework or hard evidence. They are, in this case, simply the opposites of those weathered, beaten socialists still clinging to their methodologically disastrous “evidence” of imminent bourgeoisie collapse. Or, perhaps more simply, the gold bugs are a case study in the triumph of confirmation bias over actual events.

Please follow my website if you enjoyed this article.

{kind=link}

{kind=link}

It is not my first time to visit this web page, i am

visiting this site dailly and take nice data from here all

the time.